The RWA Race: Which Blockchain Will Lead the Tokenization of Finance?

In the rapidly evolving landscape of blockchain technology, thousands of networks vie for relevance, with dozens specifically marketing themselves as real-world asset (RWA) layers. Yet amid this crowded field, only a handful truly matter as we enter an era of global tokenization. As traditional finance increasingly embraces blockchain technology, the question becomes not just which networks will survive, but which will become the foundational infrastructure for the tokenized economy of tomorrow.

Why It Matters to Pick the Right Blockchain?

The blockchain a project chooses for tokenization isn't merely a technical decision—it's strategic and potentially existential. This choice determines core characteristics like security (resistance to attacks), transaction speed (crucial for user experience), but more importantly access to a broader ecosystem of tools, services, liquidity, and mind share. When tokenizing real-world assets worth millions or billions of dollars, these are fundamental requirements.

The ultimate victor in the RWA race will be the blockchain that offers the most advanced infrastructure capable to serve as a foundation for "killer apps"—applications that drive mass adoption through exceptional utility and user experience. Currently, all indicators point to Ethereum maintaining its leadership position. And when we say Ethereum, we mean not just the main network but the entire ecosystem: Layer 2 networks like Arbitrum and Base, as well as sidechains including Polygon and Gnosis.

Ethereum

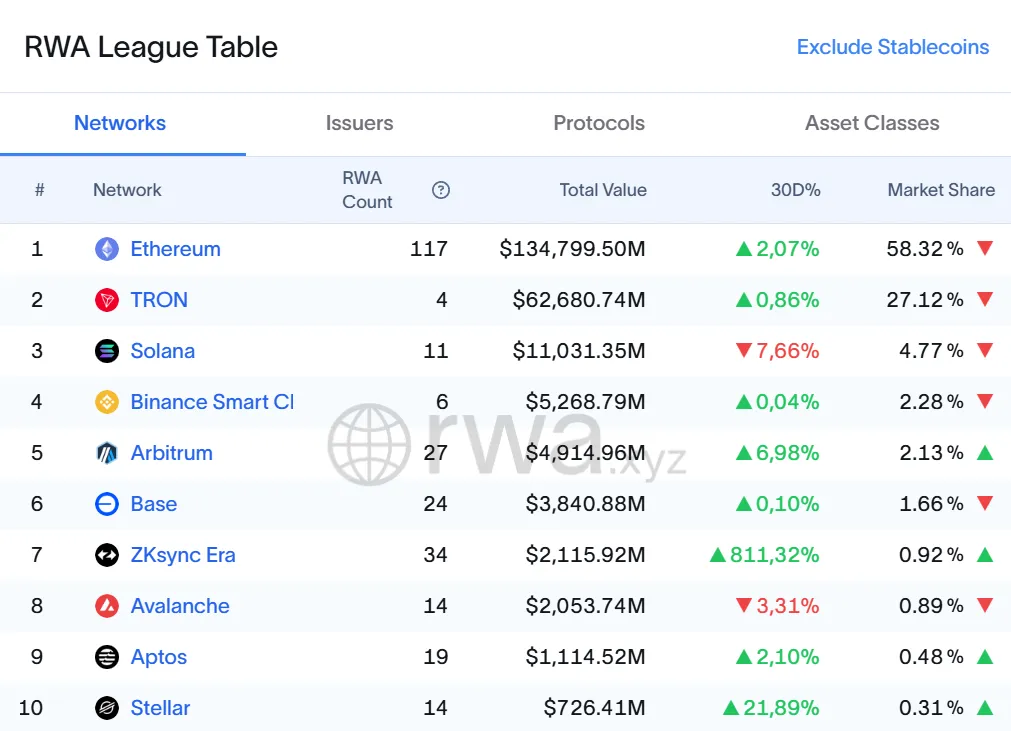

Most RWA tokenization projects and products are built on Ethereum’s mainnet, its Layer 2 networks (such as Arbitrum and Base), or its sidechains (including Polygon and Gnosis). As of this writing, the Ethereum ecosystem accounts for over 60% of the RWA market, including stablecoins, and over 80% if stablecoins are excluded.

Why Does Ethereum Maintain Its Leadership?

- The First Smart Contract Platform

Ethereum was the first blockchain to introduce smart contracts, laying the groundwork for most blockchain innovations. This first-mover advantage creates a snowball effect: the longer the ecosystem exists, the more projects choose Ethereum as the launchpad. - Security and Proven Reliability

Ethereum has demonstrated its resilience with years of uninterrupted operation. While Bitcoin might have been a better contender for RWA leadership in this regard, its architecture isn’t designed for tokenization. Ethereum’s robust and flexible framework makes it the natural choice. - Scalability Through Layer 2 Solutions

Ethereum’s focus on Layer 2 solutions, like Arbitrum and Optimism, has effectively solved scalability challenges. These networks offer fast, low-cost transactions while maintaining Ethereum’s security, making the ecosystem infinitely scalable and highly attractive for developers.

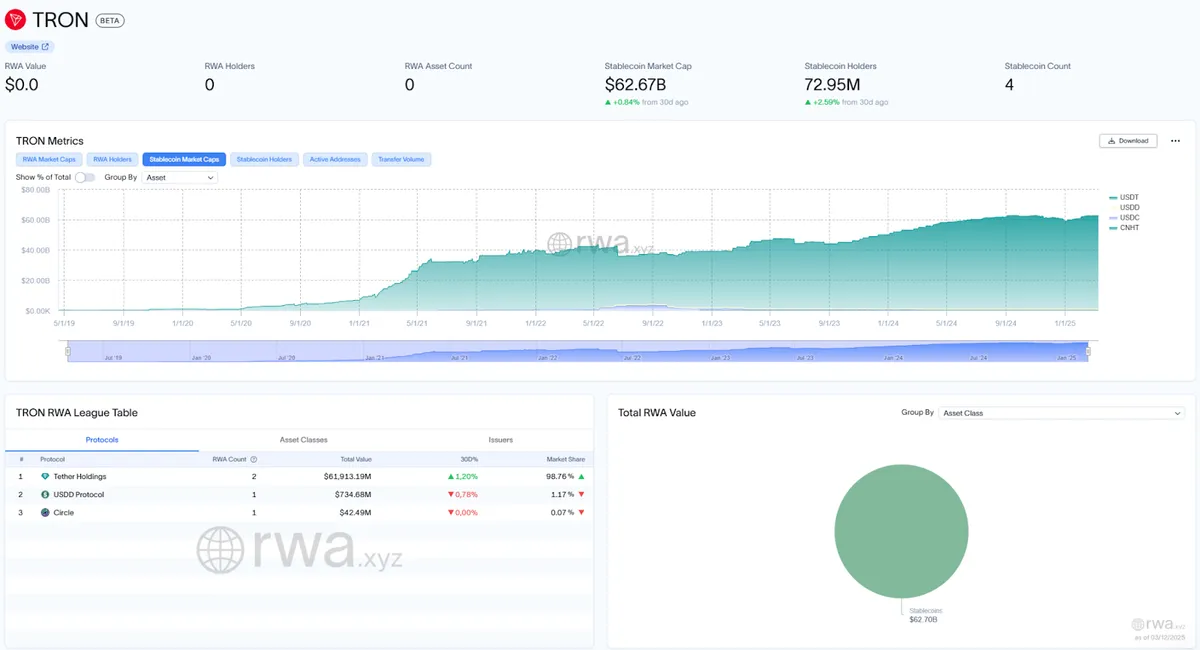

TRON

TRON holds the second position in the asset tokenization segment solely due to the stablecoin USDT, which has become particularly popular as a payment tool in the real world. TRON’s unique market fit lies in its role as a "gray zone" for financial transactions across Asia, the CIS, and the Middle East. This makes it attractive for tax optimization in payroll and other payments that are unlikely to face strict scrutiny.

However, this market fit also limits TRON’s potential. Proper asset tokenization requires close collaboration with regulators, something TRON cannot provide due to its current reputation and operational focus.

TRON’s DeFi ecosystem is virtually non-existent, consisting only of a few key products developed and maintained by the network’s founder, Justin Sun. Beyond his initiatives, the platform attracts neither significant developers nor new projects. As such, unless you are Justin Sun or plan to use the network for "gray" financial operations, TRON offers little interest for tokenization or long-term investment purposes.

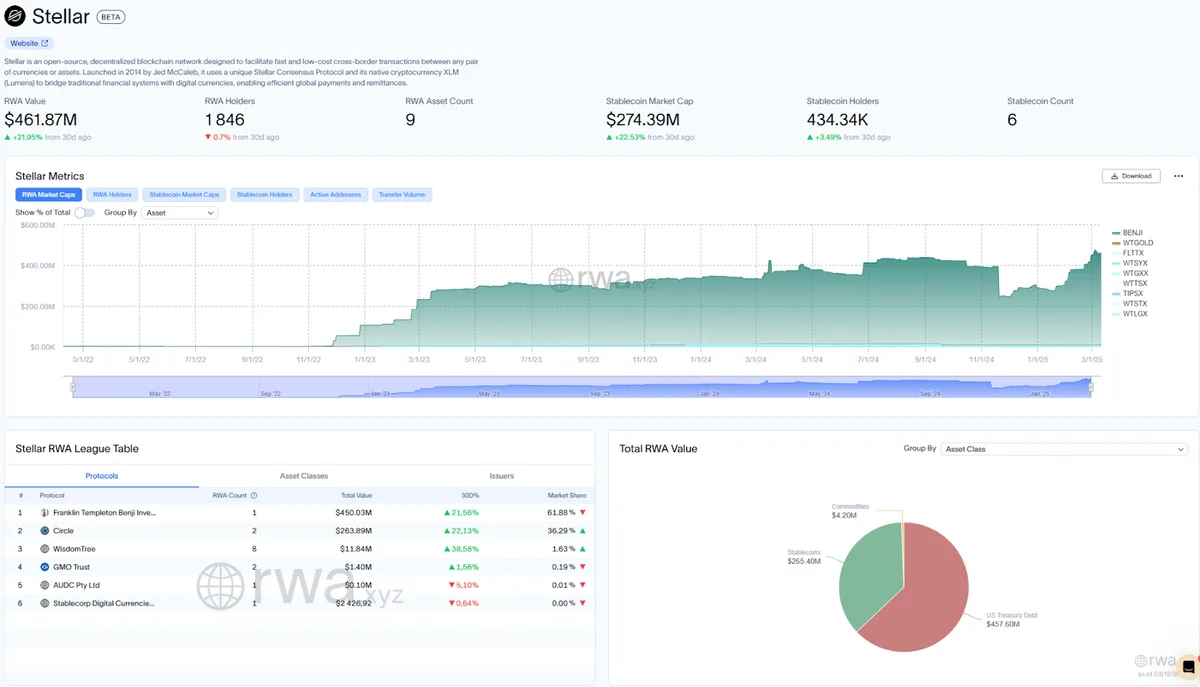

Stellar

In the realm of real-world asset tokenization, Stellar stands as Ethereum’s primary competitor, particularly when stablecoins are excluded. Launched in 2014, Stellar has focused on asset tokenization and efficient cross-border transactions from the outset.

Stellar’s strength lies in its partnerships with traditional financial institutions. Major players like MoneyGram and Circle use Stellar for cross-border payments, while Franklin Templeton has launched its RWA fund, BENJI, on the platform. Additionally, WisdomTree has implemented 13 regulated funds, including a digital gold token and a digital dollar, with a combined total of $23 million in tokenized assets. Altogether, Stellar’s tokenized asset volume is approaching $300 million.

A key architectural feature of Stellar is its trust lines mechanism. This mechanism allows users to establish direct connections with asset issuers, ensuring control over which tokens interact with their accounts.

In 2024, Stellar launched the Soroban smart contract platform, which overcomes previous limitations and enables more sophisticated decentralized applications. The Stellar Development Foundation allocated $100 million to support Soroban projects, signaling a strong commitment to strengthening its market position and attracting more developers.

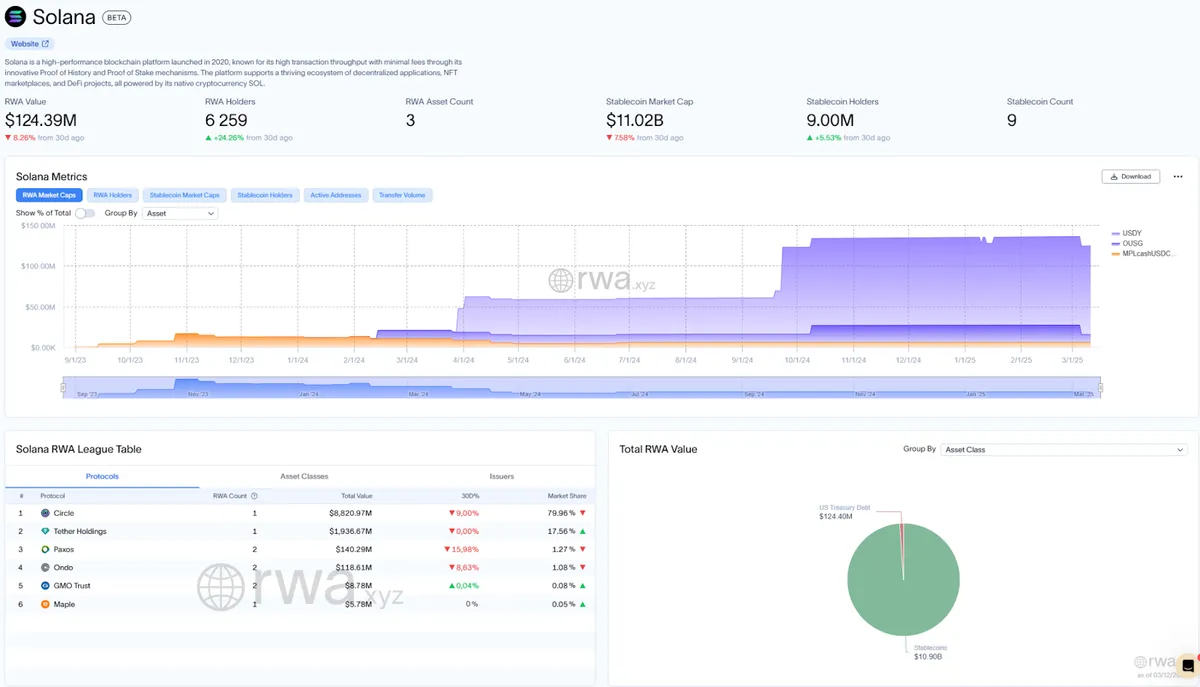

Solana

After a difficult period in 2022, when Solana was caught in the fallout from the FTX and Alameda scandals, the blockchain managed to recover and find a second wind in 2023–2024. It became a key platform for launching meme coins, which reignited attention and provided momentum for the growth of its DeFi ecosystem.

While Solana has yet to reach Ethereum’s scale, its activity and pace of innovation have surpassed those of most other blockchains. Having successfully navigated its crisis, Solana has redefined its strengths, positioning itself as a serious contender in the asset tokenization space. Currently, Solana holds approximately 4.77% of the RWA market, including stablecoins, and 1.57% when stablecoins are excluded.

RWA-Specific Blockchains

A growing number of blockchains are being designed specifically for working with real-world assets (RWA). Notably, Stellar was launched with this very purpose in mind. Its key advantage lies in its early start back in 2014 when the market was still in its infancy. This head start gives Stellar a chance to solidify its position in this niche and avoid the fate of becoming a “ghost network”—a blockchain with no activity or users.

Tokenization isn’t just about technology. Although the technical implementation is often the easiest part, the real challenge is building a vibrant ecosystem, particularly in the RWA segment, where constant engagement with regulators and institutional players is essential.

Attracting major projects and protocols to a new blockchain will only become more brutal, especially from 2025 onward, as established platforms like Ethereum continue to dominate. For any RWA protocol launched on a new blockchain, the challenge is threefold: attracting users to the product, bringing users to the network itself, and even convincing other protocols to join the same network. This process demands immense effort and resources.

For this reason, most RWA-specific blockchains are likely to remain niche solutions, unable to sustain momentum beyond short-term hype. To succeed, such platforms must offer something radically different and superior to what Ethereum or its closest competitors already provide.

Conclusion

As we've explored, the race for blockchain dominance in the RWA space isn't simply about technological superiority—it's about creating ecosystems where tokenization can thrive. Ethereum currently leads by a significant margin due to its established infrastructure, security, and developer community. While some competitors like Solana may win in specific niches, they still struggle to create a compelling alternative to Ethereum's vast ecosystem.

This article represents just one chapter from the comprehensive "RWA Thesis 2025", which offers a deeper dive into the tokenization landscape, market projections, regulatory frameworks, and emerging opportunities. If you're interested in understanding how real-world assets are reshaping the global financial system, we encourage you to read the full report for a complete picture of this transformative movement.