Is Real Estate a Liquid Asset? The Truth About Real Estate (And What's Changing in 2026)

Real estate has built more generational wealth than almost any other asset class.

But ask any property owner who has ever needed cash fast, and you will hear the same story: selling takes months, costs a fortune in commissions and fees, and forces you to give up the entire asset even when you only need a fraction of its value.

So is real estate a liquid investment? The short answer is no — traditionally, it is one of the least liquid assets you can own. But that answer is becoming more nuanced as tokenization, fractional ownership, and secondary markets reshape how investors enter and exit property positions.

In 2017, I lost one hundred thousand dollars. Not to a scam, not to fraud — to my own emotions. I sold my car, put everything into mining, made money, and lost almost everything on one emotional trade. That was the most expensive lesson of my life, and it taught me something critical: the ability to exit an investment when logic tells you to exit — not when the market allows you to — is everything.

This guide breaks down real estate liquidity honestly: what makes property illiquid, the real financial costs of that illiquidity, how liquidated damages and exit penalties compound the problem, and what modern alternatives look like for investors who want real estate returns without the capital trap.

What Makes an Asset "Liquid"?

Before answering whether real estate is liquid, it helps to define what liquidity actually means in practical terms.

An asset is considered liquid when it can be converted into cash quickly, at or near its fair market value, without significant transaction costs. Cash itself is the most liquid asset. Publicly traded stocks are highly liquid — you can sell 50 shares of Tesla in 30 seconds and have the proceeds in your brokerage account the same day.

Liquidity exists on a spectrum. At one end sits cash and money market instruments. In the middle are publicly traded securities, bonds, and some commodities. At the far illiquid end sit assets like fine art, private equity stakes, and — historically — real estate.

Three factors determine where an asset falls on this spectrum: how fast you can sell it, how much it costs to sell it, and how much you lose relative to fair value when selling under time pressure. Real estate performs poorly on all three measures.

Why Real Estate Scores Low on Every Liquidity Metric

Time to sell. According to Zillow's market data, the average time to sell a house in the US is 47 to 62 days from listing to close — and that is in the world's most liquid real estate market. HomeLight reports that as of late 2025, homes spent an average of 64 days on the market before going under contract, with an additional 41 days needed to close. In less liquid international markets, timelines stretch dramatically: in Bali, the average villa sale takes six months to a year. Montenegro is similar. This assumes you find a buyer willing to pay your asking price — which leads directly to the next problem.

Transaction costs. Selling property is expensive. According to Bankrate's commission data, the national average real estate commission in the US is 5.57% of the sale price — split between the listing agent (2.82%) and the buyer's agent (2.75%). A 2026 survey by Clever Real Estate confirms that total commissions range from 5% to 6%, with some markets reaching higher. Add notary fees, transfer taxes, legal reviews, staging and marketing costs, and you are looking at 6–10% of the property's value consumed by the transaction itself — before you receive a single dollar.

Price impact under pressure. When you need money urgently, buyers sense it. Experian's 2025 housing analysis notes that nearly 1 in 5 listings in 2025 had price cuts — the most in a decade. Negotiation typically shaves another 5–15% off the asking price for motivated sellers. Combine that with transaction costs, and an urgent sale can destroy 15–25% of your asset's value. Not because the property is worth less, but because the market is slow and the seller has no leverage.

Indivisibility. Perhaps the most underappreciated liquidity problem: you cannot sell a portion of a traditional property. Need $10,000 but your apartment is worth $100,000? You sell everything or nothing. There is no middle ground. Compare that to stocks, where you can sell exactly the number of shares you need and keep the rest of your position intact.

Is Real Estate a Liquid Investment? A Realistic Assessment

The honest answer is that traditional real estate is an illiquid investment. It sits near the bottom of the liquidity spectrum, alongside assets like private business equity, collectible art, and venture capital holdings.

This does not make real estate a bad investment. Illiquidity is precisely what creates many of the return premiums that property investors enjoy. You are being compensated — through higher yields, tax advantages, and appreciation potential — for accepting the difficulty of converting your position to cash.

The problem is not that real estate is illiquid. The problem is that most investors underestimate what illiquidity costs them until they actually need to exit.

The Hidden Cost of Illiquidity: What Investors Actually Lose

Consider a practical scenario. You invested $50,000 in a property generating 8% annual rental yield. After two years, you need cash — maybe for a business opportunity, a family emergency, or simply because you want to rebalance your portfolio.

Here is what happens in a traditional sale:

You list the property. Your realtor estimates three to six months to close. Meanwhile, your cash need persists. A buyer appears but negotiates 10% below asking. You accept because you need the money. After realtor commissions (5.57% — the national average per Clever Real Estate), notary and legal fees (1–2%), and the negotiated discount (10%), you receive approximately $41,500 from your $50,000 property — a 17% haircut just to access your own capital.

That 17% loss wipes out two full years of rental income. Your effective return over the entire holding period drops from 8% annual to near zero — or negative, once you factor in maintenance, insurance, and management costs during ownership.

This is the illiquidity penalty, and it is far more common than most real estate marketing materials acknowledge.

Liquidated Damages in Real Estate: The Contractual Side of Exit Costs

Beyond market-driven illiquidity costs, real estate investors face contractual penalties that further restrict their ability to exit. Liquidated damages clauses are among the most common and least understood obstacles to real estate liquidity.

What Are Liquidated Damages in Real Estate?

Liquidated damages are pre-agreed financial penalties written into real estate contracts that apply when one party fails to fulfill their obligations — most commonly, when a buyer backs out of a purchase agreement. According to the National Paralegal College's legal analysis, liquidated damages provisions are "generally considered valid as long as the situation is such that actual expectation damages are difficult to measure and if the amount of liquidated damages called for is a reasonable approximation of the seller's actual damages."

In a typical residential transaction, the liquidated damages clause specifies that if the buyer defaults, the seller keeps the earnest money deposit as compensation. The amount varies by state and deal type: in California, the California Association of Realtors® standard form caps liquidated damages at 3% of the purchase price. In Washington State, RCW 64.04.005 caps earnest money forfeiture at 5% of the purchase price for standard residential transactions. In commercial real estate and development deals, liquidated damages can be substantially larger and more complex.

How Liquidated Damages Affect Investors

For investors, liquidated damages create a multi-sided problem that compounds the illiquidity of the underlying asset.

As a buyer trying to exit before closing: If market conditions change or you find a better opportunity after signing a purchase agreement, walking away means forfeiting your deposit. On a $200,000 property with a 3% earnest money deposit, that is $6,000 lost — not because of market performance, but because the contract structure penalizes flexibility. As Seidman Law Group notes, "a rapidly escalating real estate market could devastate a buyer that breaches the purchase and sale agreement" since the seller may pursue actual damages beyond the deposit if the contract allows it.

As a seller in a development or construction deal: Many off-plan and construction investment agreements include clauses where the developer can charge liquidated damages if the investor attempts to exit before project completion. These can range from forfeiture of installments already paid to additional penalty fees. The investor's capital is effectively locked until the developer's timeline is met — which may be years.

As a landlord under lease obligations: Selling a tenanted property introduces additional complexity. Breaking lease terms to sell vacant possession can trigger liquidated damages owed to the tenant. Selling with tenants in place often means accepting a lower price because the buyer pool narrows to other investors only.

Enforceability: Can Liquidated Damages Be Challenged?

Not all liquidated damages clauses hold up in court. According to analysis by Finney Law Firm, Ohio courts use a three-part test to evaluate enforceability, and courts will not enforce provisions that function as a "penalty" rather than a genuine pre-estimate of damages. The key legal standard across most US jurisdictions requires that: (1) actual damages were difficult to estimate at the time of contracting, (2) the liquidated amount is a reasonable approximation of anticipated damages, and (3) the clause was not designed as a punishment.

However, challenging a liquidated damages clause in court is itself expensive and time-consuming — adding yet another layer of cost to an already illiquid exit.

Liquidated Damages vs. Illiquidity Premium

It is worth distinguishing between liquidated damages (contractual penalties) and illiquidity costs (market friction). Both reduce your net proceeds when exiting, but they operate differently.

Liquidated damages are predetermined, written into contracts, and theoretically negotiable before you sign. Illiquidity costs are market-driven, unpredictable, and largely outside your control. A sophisticated investor plans for both — but few real estate deals are structured to minimize either.

How Different Real Estate Investment Types Compare on Liquidity

Not all real estate investments carry the same liquidity profile. Here is a realistic comparison across the major categories.

Direct Property Ownership

Liquidity: Very low. Market data shows three to twelve months to sell, depending on market conditions. Full transaction costs of 6-10%+ apply. Cannot sell a portion. This is the classic illiquid real estate position.

Real Estate Investment Trusts (REITs)

Liquidity depends entirely on the REIT type, and the distinction matters more than most investors realize.

Publicly traded REITs are highly liquid. They trade on major exchanges like the NYSE and NASDAQ, and according to Investor.gov (SEC), investors can buy and sell shares at market price during trading hours — just like stocks. There are over 200 publicly traded REITs available, offering instant portfolio exposure to real estate without any lock-up period.

Non-traded REITs are a different story entirely. These do not trade on exchanges, making them inherently illiquid. LegalClarity's REIT analysis explains that non-traded REITs may offer Share Repurchase Programs (SRPs), but these are discretionary, not guaranteed, and typically capped at 2% to 5% of outstanding shares quarterly. Lock-up periods of three to eight years are common. The real-world consequences of this illiquidity became clear in 2022-2023 when major non-traded REITs like Blackstone's BREIT and Starwood's SREIT were forced to limit investor withdrawals — or "gate" redemptions — because requests exceeded monthly limits. According to CRE Daily, non-traded REITs have now processed $56 billion in redemptions since that crisis began, with BREIT only fully lifting its withdrawal cap by March 2024. That is a sobering lesson about "liquid" real estate investments that turned out to be anything but.

Real Estate Crowdfunding

Liquidity: Low to moderate. Most platforms have holding periods of one to five years. Some offer secondary markets, but trading volume is typically thin and discounts of 10–20% are common for early exits.

Tokenized Real Estate (Fractional Ownership)

Liquidity: Moderate and improving. Properties are divided into digital tokens representing fractional ownership. Investors can list tokens on platform-operated secondary markets and sell portions of their position without exiting entirely. Transaction times range from minutes to 48 hours depending on demand. Transaction costs are typically 2–5%, compared to 8–15% for traditional sales.

This last category represents the most significant shift in real estate liquidity in decades, and it is worth examining in detail.

How Tokenization Is Solving the Real Estate Liquidity Problem

The core innovation of tokenized real estate is simple: take a property worth $500,000, divide it into 10,000 digital tokens at $50 each, and let investors buy and sell these tokens independently. This is the approach used by platforms like Binaryx, where every property is divided into tokens typically priced between $30 and $50.

This structure solves all four of the traditional liquidity problems outlined earlier.

Fractional Selling

You own 200 tokens worth $10,000 and need $2,000? Sell 40 tokens. Keep the remaining 160. Continue earning rental income on your remaining position. This is structurally impossible with a physical apartment or villa — where you either sell everything or hold everything.

Speed of Exit

On platforms with active secondary markets, the average token sale time ranges from 40 minutes to 48 hours. These are real numbers from the Binaryx secondary market, where hundreds of investors participate monthly and all transactions are publicly visible in real time. Compare that to six to twelve months for traditional property. The speed difference is not incremental — it is a category change.

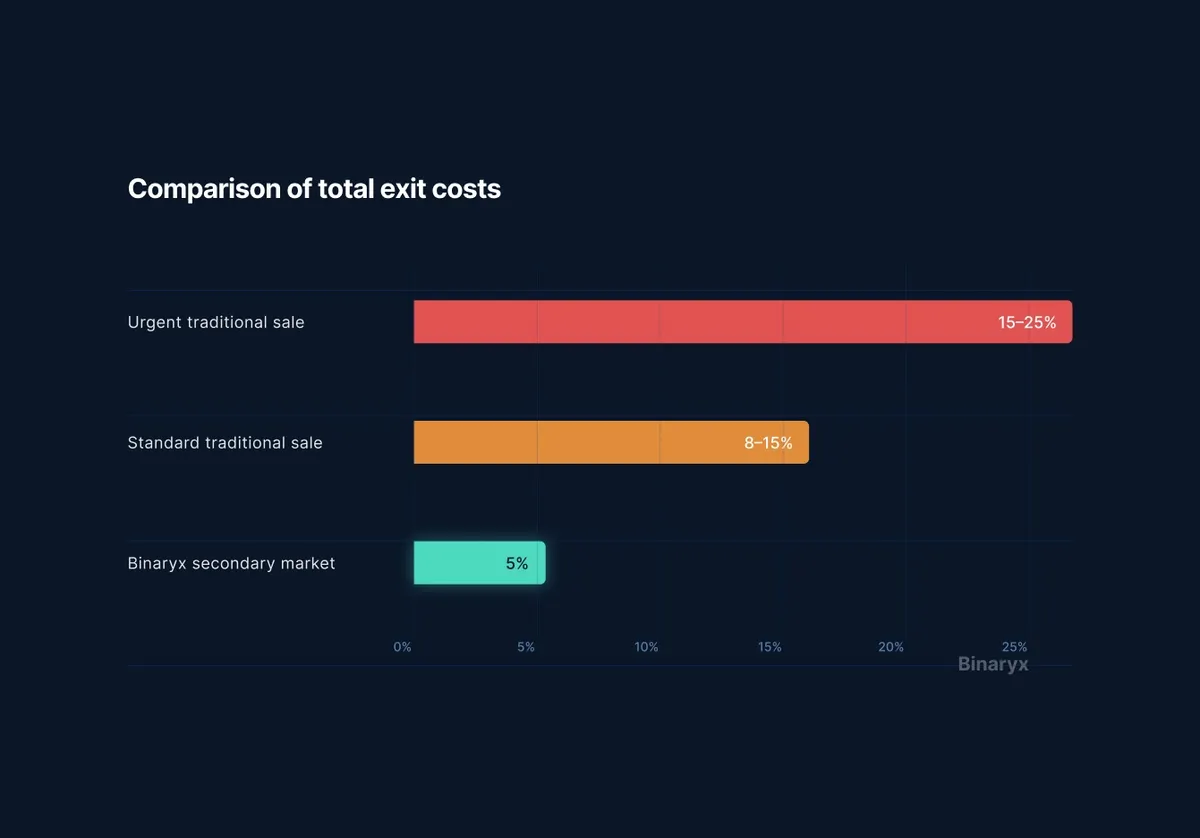

Reduced Transaction Costs

Traditional real estate sales cost 8–15% in combined commissions, fees, taxes, and negotiation discounts. Tokenized secondary market transactions on Binaryx carry a total cost of 5% — consisting of a 2% platform commission plus a 3% discount to the next buyer. On a $10,000 position, that is $500 versus $800–$1,500 or more with traditional real estate. And you only sell the portion you need.

How does that compare?

Price Transparency

Every transaction on a token-based secondary market is recorded and publicly visible. Buyers and sellers can see recent trade history, current listings, and market depth. There is no information asymmetry between a desperate seller and an opportunistic buyer — which is precisely what destroys value in traditional urgent sales.

What the Full Comparison Looks Like

| Factor | Traditional Property | REITs (Publicly Traded) | REITs (Non-Traded) | Tokenized Real Estate |

|---|---|---|---|---|

| Time to sell | 6–12 months | Instant (market hours) | Months to years (gated) | 40 min – 48 hours |

| Transaction costs | 8–15% | Brokerage fees (~0.1%) | Redemption penalties (varies) | 2–5% |

| Can sell a portion | No | Yes (sell shares) | Limited | Yes (sell tokens) |

| Minimum investment | $50,000–$500,000+ | $1–$100 (per share) | $2,500–$50,000 | $50 (per token) |

| Direct property ownership | Yes | No (pooled fund) | No (pooled fund) | Yes (fractional co-ownership) |

| Price control | Limited under pressure | Market-driven | NAV-based (opaque) | Seller sets listing price |

| Income from asset | Rental yield | Dividend (90% payout req.) | Dividend (variable) | Rental yield (direct) |

| Liquidated damages risk | Common in contracts | None | Early redemption penalties | Minimal — no lock-up |

Smart Strategies for Managing Real Estate Liquidity

Whether you invest in traditional property or tokenized alternatives, liquidity management should be part of your investment thesis from day one — not something you think about only when you need cash.

Buy at a Discount When Others Sell Under Pressure

On secondary markets, tokens sometimes list at 3–7% below face value. Before buying, analyze why the discount exists. If it is a temporary issue being resolved — a management company transition, a seasonal dip in rental demand — you are buying an income-generating asset below market.

Here is the math: a token with a $50 face value selling at $48.50, on a property yielding 9% annually, gives you an effective return of 11.6%. Plus you gain potential price recovery back to face value once the temporary issue resolves. This kind of opportunistic buying is only possible when a liquid secondary market exists.

Rebalance Without Full Liquidation

Traditional investors are stuck: hold everything or sell everything. With fractional positions, you can shift allocation gradually. Own $10,000 in a property yielding 7%? A new opportunity appears at 9–10%? Sell a portion of your existing tokens and redeploy — in hours, not months.

Take Profits in Stages

A construction-phase property completed and your tokens appreciated 20%? Sell a portion to lock in profit, keep the rest for ongoing rental yield, and reinvest the freed capital into the next opportunity. Our internal calculations show that reinvesting gains adds 2–3% to annual portfolio returns over time. This is compound interest applied to real estate — something that was structurally impossible before fractional ownership.

Plan Your Exit Before You Enter

The most important liquidity strategy is the simplest: decide how and when you will exit before you invest. What is your target holding period? What conditions would trigger an early exit? What would it cost to exit under different scenarios? If the answers involve "wait six months and hope for a buyer," you are accepting more illiquidity risk than you may realize.

As one Binaryx investor, Evgeny, put it after 10+ years of offline real estate experience: "My offline real estate was yielding 6–7% annually. Here I see 11%+, and most importantly — I can sell a portion in a day, not a year. The key factor was the ability to exit." For Evgeny, just like for me after that lesson in 2017, the ability to exit is not just convenience. It is peace of mind.

The Honest Limitations of Tokenized Real Estate Liquidity

No liquidity solution is perfect, and intellectual honesty demands acknowledging the constraints.

Secondary market depth depends on the platform's investor base. Smaller platforms with fewer participants will have thinner markets and longer sale times. Liquidity for specific properties can vary — tokens for well-performing rental properties tend to sell quickly, while tokens for properties with management issues or delayed payouts may sit on the market longer. As another Binaryx investor, Elena, accurately observed: "On the secondary market, some properties do not generate profit due to issues with the management company." She is absolutely right. That is normal market dynamics.

This is actually a healthy market signal. When a management company delays reporting or underperforms on rental payouts, investor caution is rational. The tokens are not "stuck" — the market is correctly pricing uncertainty. What matters is how the platform responds.

In our case, when a few Bali units had inconsistent payouts from the operator, we took three concrete steps: enforced contractual obligations with legal and operations experts, initiated operator replacement with co-owners where possible, and moved units under a more established operator. The market typically unfreezes after the first clean reporting and payout cycle under the new operator. That is the proof investors wait for — and it is rational.

Tokenized real estate also carries platform risk. Your liquidity depends on the platform's continued operation and the integrity of its smart contracts. This is a different category of risk than traditional real estate, and it should be weighted accordingly in your diversification strategy. At Binaryx, we address this through a DAO LLC legal structure where token holders have governance rights and voting power — meaning investors are not dependent on a single entity's decisions.

Real Estate Liquidity by Country: Where Exit Is Hardest

Liquidity varies dramatically depending on where you invest. Understanding local market dynamics is essential for setting realistic exit expectations.

Bali, Indonesia. One of the most popular emerging markets for villa investment, yet among the most illiquid for foreign sellers. Foreigners cannot hold freehold title (only leasehold or nominee structures), which limits the buyer pool. Average sale timelines run six to eighteen months for villas, and foreign investors often face additional legal complexity that slows transactions further. The resort rental market is strong, but converting that property to cash requires navigating Indonesian property law — a process that many foreign investors underestimate.

Montenegro. A growing destination for European property investors, but with a relatively thin market. Luxury coastal properties in Budva or Kotor may sell within three to six months during peak season, but off-season listings can sit for a year or more. The small market size means fewer active buyers at any given time.

Turkey. Higher market volume than Montenegro, but currency volatility (the Turkish lira has lost significant value against the US dollar and euro in recent years) introduces pricing complexity. Selling in local currency may mean receiving less in real terms than you paid, even if the nominal property value increased.

United States. Generally the most liquid major real estate market, with established MLS systems, standardized processes, and deep buyer pools. Clever Real Estate's research shows the typical US city has 2.8 months of housing supply, with median days on market ranging from 13 days in Grand Rapids, Michigan, to 69 days in Miami. Still, total transaction costs of 5–6% in commissions alone — plus taxes, legal fees, and potential negotiation discounts — and the inability to sell partially remain.

Western Europe (Germany, France, Netherlands). Moderate liquidity with well-regulated markets but high transaction taxes. German property transfer tax alone runs 3.5–6.5% depending on the state, on top of notary and agent fees. France adds notary fees of approximately 7–8% for older properties.

For investors who want geographic diversification without being locked into any single market's liquidity constraints, fractional models offer a structural advantage: your exit mechanism is the platform's secondary market, not the local property market.

Explore properties currently available on the Binaryx secondary market — some at discounts. Analyze why the discount exists. Make your own decision. Browse the platform →

Have questions? Book a free consultation with a Binaryx financial advisor to understand what suits you: rental properties, construction projects, or secondary market opportunities at a discount. Schedule a call →

Is Real Estate Liquid? The Bottom Line for 2026

Traditional real estate remains one of the most illiquid mainstream asset classes. Selling takes months, costs 8–25% depending on urgency, cannot be done partially, and often involves contractual penalties like liquidated damages that further restrict your flexibility.

But the binary framing — "real estate is illiquid, stocks are liquid" — is becoming outdated. Tokenization and fractional ownership platforms are creating a middle category: real estate with moderate liquidity, where investors can sell portions of their positions in hours rather than months, at a fraction of the traditional exit cost.

The fundamental value proposition of real estate has not changed. Property still generates rental income, appreciates over time, hedges inflation, and provides diversification benefits that purely financial assets do not. What is changing is the structural penalty investors pay for accessing those benefits.

Tokenized real estate is not perfect. There are risks — management companies, construction delays, demand volatility. But it gives you what traditional real estate never will: control over your exit and a voice in decision-making through DAO governance.

Real estate does not need to become as liquid as stocks to represent a massive improvement over the status quo. It just needs to stop trapping your capital for months every time you need flexibility. For a growing number of investors, that barrier has already fallen.

Frequently Asked Questions About Real Estate Liquidity

Is real estate considered a liquid or illiquid asset?

Real estate is classified as an illiquid asset. Unlike stocks or bonds, property cannot be converted to cash quickly without significant transaction costs. Traditional sales take 47 to 62 days in the US at minimum and cost 5.57% in commissions plus additional fees, totaling 8–15% or more. However, newer models like tokenized real estate and publicly traded REITs offer improved liquidity compared to direct property ownership.

What are liquidated damages in real estate?

Liquidated damages are pre-agreed financial penalties in real estate contracts that apply when one party breaches the agreement — most commonly when a buyer backs out. The penalty is typically equal to the earnest money deposit, which ranges from 1–5% of the purchase price depending on the state and contract terms. These clauses are enforceable when they represent a genuine pre-estimate of damages rather than a penalty.

What is the difference between real estate liquidity and liquidated damages?

Real estate liquidity refers to how easily and quickly you can convert a property investment into cash. Liquidated damages are a separate legal concept — pre-agreed financial penalties written into real estate contracts that apply when one party fails to meet their obligations. Both affect your total cost of exiting, but liquidity is a market condition while liquidated damages are a contractual provision.

Can I sell part of a real estate investment without selling the whole property?

Not with traditional direct ownership. If you own an apartment or villa, you must sell the entire asset or nothing. However, tokenized real estate platforms like Binaryx divide properties into digital shares (tokens) that can be traded independently. This allows you to sell 20% of your position while keeping the remaining 80% and continuing to earn rental income.

What is the most liquid type of real estate investment?

Publicly traded REITs offer the highest liquidity among real estate investments — shares trade on stock exchanges during market hours, just like regular stocks. However, publicly traded REITs do not provide direct property ownership; you own shares in a pooled fund, not a specific property. For investors who want direct fractional ownership with moderate liquidity, tokenized real estate platforms offer a middle ground.

How long does it take to sell tokenized real estate?

On active platforms with established secondary markets, average sale times range from 40 minutes to 48 hours for tokens tied to well-performing properties. Tokens for properties experiencing management issues or reporting delays may take longer, as buyers apply additional due diligence before purchasing.

Are there penalties for selling real estate investments early?

With traditional property, early exit costs include realtor commissions (5–6%), legal fees, transfer taxes, and potential liquidated damages if you are breaking a contractual obligation. Many off-plan and construction deals also include penalties for investor withdrawal before project completion. Non-traded REITs may gate redemptions or impose early withdrawal penalties. Tokenized real estate typically has lower exit costs (2–5% total) and no contractual lock-up penalties, though secondary market pricing depends on supply and demand.

How do REITs compare to tokenized real estate for liquidity?

Publicly traded REITs offer instant liquidity (buy/sell during market hours) but no direct property ownership — you hold shares in a fund, not a specific asset. Non-traded REITs offer potential higher yields but are illiquid, with lock-ups of 3–8 years and redemption caps of 2–5% quarterly. Tokenized real estate offers a middle ground: direct fractional ownership of specific properties, with secondary market exit in hours rather than months, and total transaction costs of 2–5%.

Can you lose money on liquidated damages in real estate?

Yes. If you sign a purchase agreement and later decide not to close, you will typically forfeit your earnest money deposit (1–5% of the purchase price). In some cases, if the contract allows, the seller may pursue actual damages beyond the deposit — which could be substantially more. Commercial real estate contracts and off-plan development agreements often carry even higher liquidated damages provisions. Always review liquidated damages clauses with a real estate attorney before signing.