Beat Inflation: Real Estate is the Hedge That Works

Inflation has become the headache of recent years, touching nearly every corner of the world. Sure, it’s been a constant companion in economic discussions, but it surged into the spotlight after the COVID-19 era when central banks pumped out waves of money to revive stalled economies. Prices soared over the last four years and are still climbing today, though driven by different forces. So, how can one protect against this relentless rise? Real estate is one of the most effective answers — it pays you while it protects you, generating passive income from real estate even as prices climb.Let's dive in and find out.

Unstoppable Decline of Your Currency’s Value

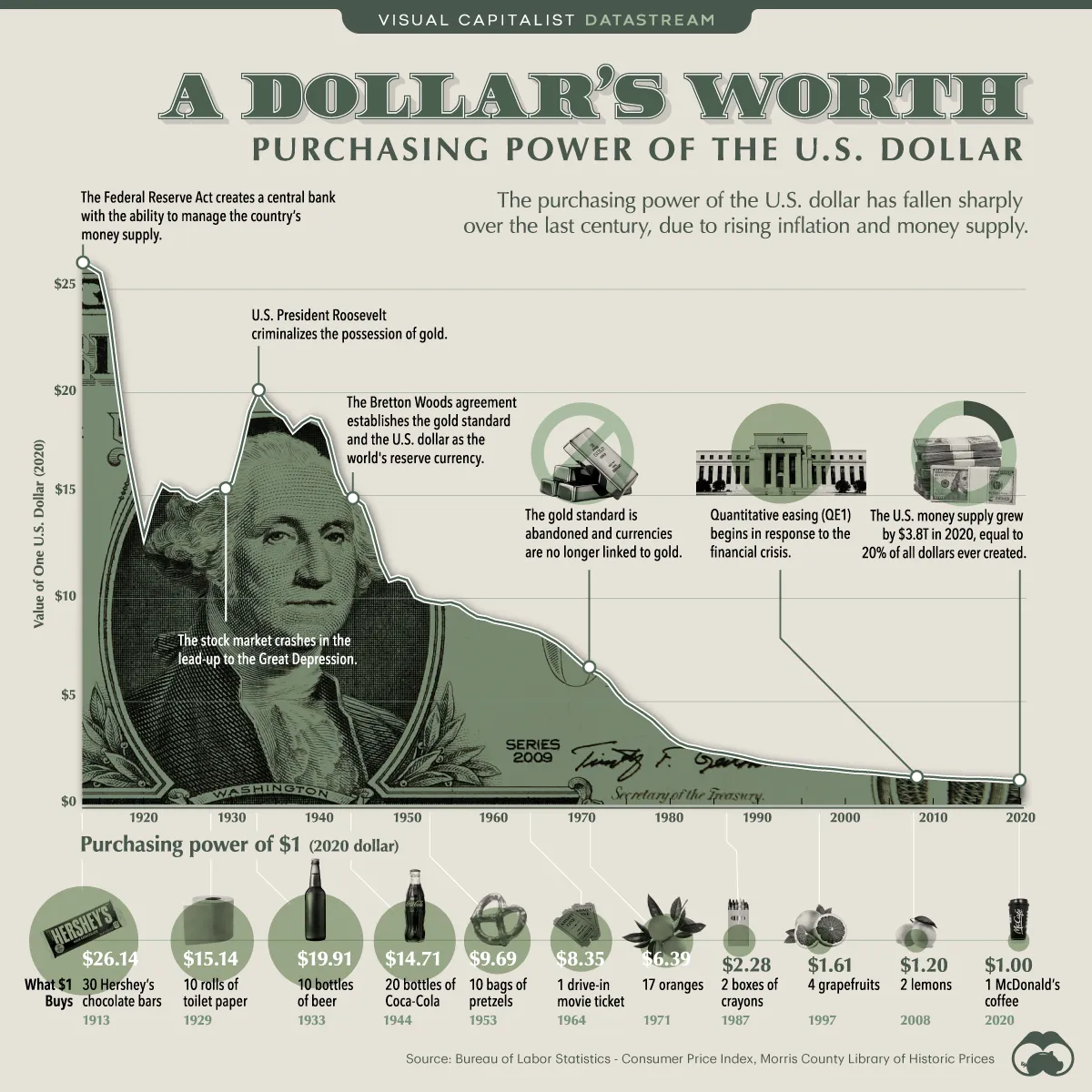

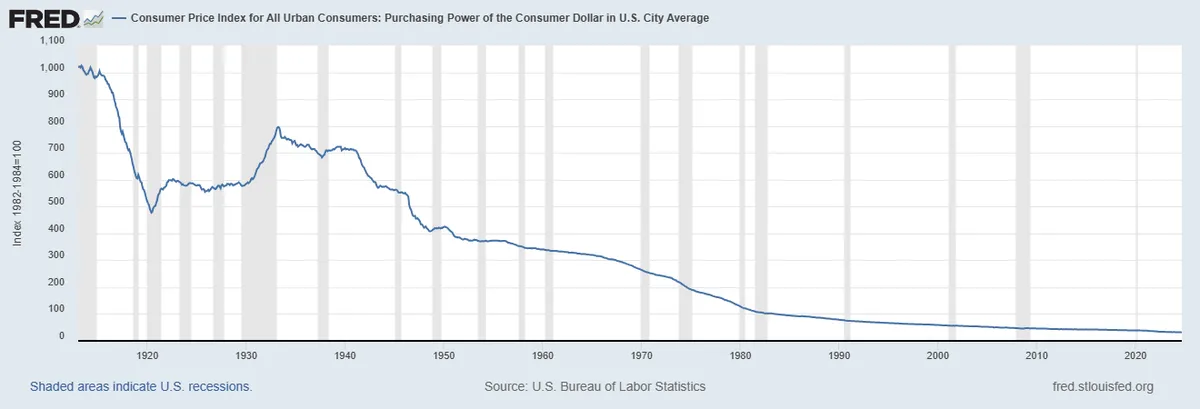

Everyone knows inflation and its causes—it’s a topic that spares no one, especially those with some extra money to safeguard. So, let’s skip the basics and visualize the sheer impact. Consider the U.S. dollar, hailed as the world’s strongest currency. You've probably seen charts showing the decline of its purchasing power over the last century. This one shows that one dollar could have been repurchased then and now needs nearly twenty-five to match the same worth.

If we look at more actual data and calculate precise percentages, it hits even harder. From 1914 to 2024, the dollar has lost a staggering 96.8% of its value.

If the so-called stable dollar has taken such a hit, imagine what’s happened to other, less resilient currencies. More importantly, think about what’s coming in the next decade. Without proper strategies, currency devaluation isn't just a historical issue; it's a future one, too.

Common Inflation Hedges: Gold, Bonds, Bitcoin, Stocks, and Real Estate

Gold

The timeless go-to. People have trusted gold for centuries as a store of value, significantly when paper money weakens. It doesn’t generate income but holds its worth as currencies depreciate. Historically, gold prices tend to rise during inflation spikes.

Treasury Bonds

Classic government bonds offer fixed interest payments over a set period. They are considered safe and stable—primarily when issued by the U.S. or certain European governments. However, their fixed returns can suffer during inflation as real earnings decline. Treasury Inflation-Protected Securities (TIPS) provide an alternative; their principal value adjusts with the Consumer Price Index (CPI), rising as inflation increases.

Bitcoin

A newer contender, Bitcoin has been touted as digital gold. Its capped supply of 21 million coins ensures scarcity. In recent years of rapid inflation, Bitcoin gained attention as a potential inflation hedge, though its volatility can deter traditional investors. Whether it is a true hedge remains debated—only time will tell.

Stocks

Equities may not seem like a primary inflation hedge, but many companies manage to pass increased costs to consumers, protecting their profit margins. Stocks with strong fundamentals, particularly in sectors like energy and consumer goods, can help offset inflation’s impact over time.

Real Estate

It is a classic that has proven its worth during inflationary periods. Property values and rental income typically rise with inflation, making real estate a tangible shield against currency devaluation. It provides a dual benefit: asset appreciation and steady rental income.

What Is the Best Inflation Hedge?

Choosing the best inflation hedge depends on your investment horizon, personal preferences, and available capital. Some options work well for long-term wealth preservation, while others provide quicker responses to rising prices. Knowing what fits your needs and strategy is key to protecting your purchasing power.

Gold has long been a trusted store of value, particularly over extended periods. Historical data shows its true strength as an inflation hedge emerges over decades. On the other hand, stocks adapt better to shorter and medium-term inflation. The S&P 500 has averaged a 10% annual return over the past century, thanks to companies passing on rising costs to maintain earnings. For those looking at a newer option, Bitcoin holds promise due to its capped supply, although its volatility and short history mean it’s still finding its place as an inflation hedge.

Treasury Inflation-Protected Securities (TIPS) adjust with inflation and are worth considering for an easy-to-go approach. Real estate stands out for its tangible value and consistent returns. Property values and rental income often move with inflation, making real estate a solid option for protection and income.

Why Pick Real Estate as an Inflation Hedge?

Real estate stands out as an inflation hedge for several reasons, starting with income generation. Rental properties bring in consistent income, which usually rises with inflation, creating a dual benefit—steady cash flow and long-term value growth. Unlike paper assets, real estate is tangible and holds intrinsic worth. The idea of “depreciating debt” adds another layer of appeal: as inflation pushes prices higher, mortgage payments become cheaper in real terms. Over time, you pay off that debt with dollars worth less than when you first borrowed it, turning inflation from a threat into an advantage.

Also, a few other investments let you control a significant asset using a relatively small amount of your money. Sometimes, you might only need 5% down. If home prices rise by 5%, you've effectively doubled your initial investment. This ability to leverage other people’s money means gains are amplified—something that can’t be matched by stocks, bonds, or even gold. Plus, your properties can serve as collateral for more loans, basically allowing you to expand your real estate portfolio in progression.

Yes, there are disadvantages. Real estate isn't liquid; selling takes time, and transaction costs cut into profits. Maintenance, taxes, and insurance add expenses, and leverage can turn sour if property prices fall. But these drawbacks pale when weighed against the income, tangible value, and leverage benefits.

Modern Approaches to Inflation-Proof Real Estate Investing: REITs, ETFs, Crowdinvesting

If you’ve chosen real estate as your hedge against inflation, know there are options even if you’re not ready to buy an entire property. Modern methods make real estate investing accessible, even with a smaller budget.

REITs (Real Estate Investment Trusts) let you invest in income-generating properties without buying or managing them. You purchase shares and earn dividends from properties owned by the trust. It’s a straightforward way to secure passive income from real estate without diving into property upkeep.

Real estate ETFs and mutual funds take a broader approach. They hold a mix of REITs, property stocks, and related bonds, spreading out risk and giving exposure to the real estate sector. It’s conservative, straightforward, and passive, perfect for those who want a set-and-forget strategy with steady, if modest, returns.

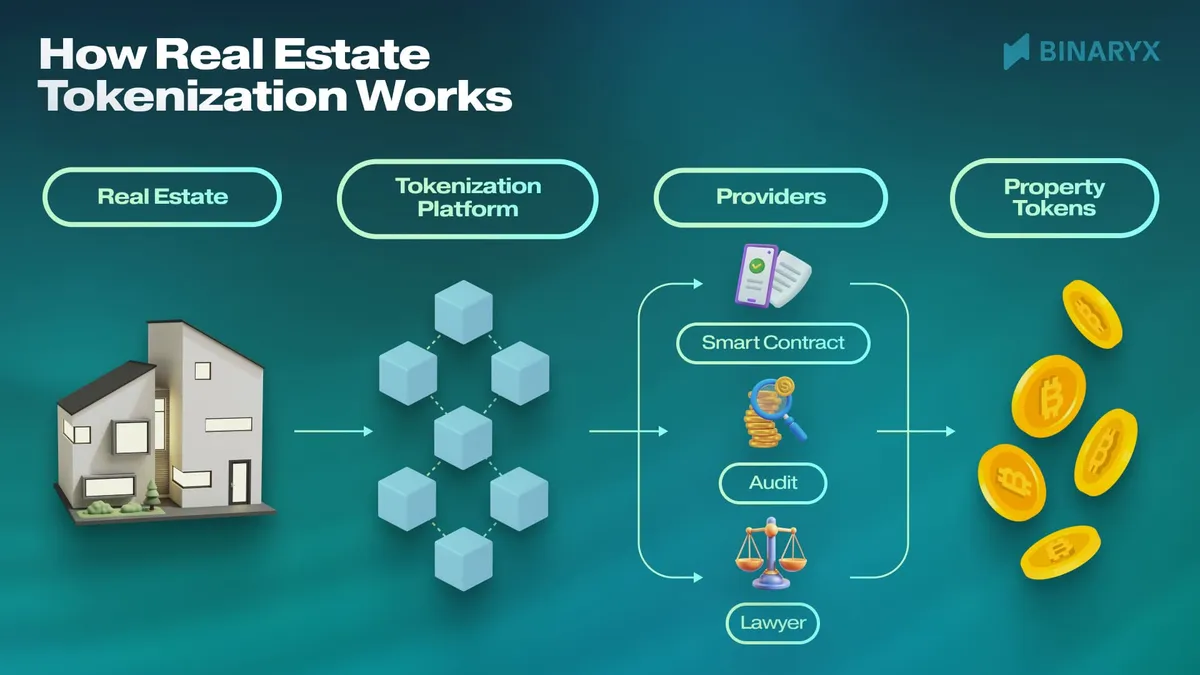

Crowdinvesting opens doors to co-investing and co-ownership. Pool your money with other investors to back significant real estate ventures. Professionals manage these projects, so you’re not involved beyond tracking updates and collecting income. Tokenization brings a tech twist there. Properties get divided into digital tokens representing ownership shares traded on a blockchain. You buy tokens and own a piece of the property’s rental income or resale profits. Smart contracts handle payments, making it a seamless, hands-off investment.

Protect Against Inflation with Binaryx

If you're looking for an effective way to hedge against inflation, the Binaryx platform offers a modern approach to real estate investing through tokenization. Binaryx simplifies access to prime real estate by turning properties into digital tokens, each representing a fraction of ownership. Here’s how it works: the platform sets up a Special Purpose Vehicle (SPV), structured as an LLC under the Wyoming DAO LLC Act, to legally hold the property title. This ensures each token carries legitimate ownership rights. Tokens are stored on the blockchain, and smart contracts manage rental income distribution and ownership terms, creating a seamless, automated investment experience.

You can buy tokens starting at $500 and get a profit automatically. The Binaryx Platform handles property management, so investors only need to track their shares and receive automated rental payouts. Additionally, a secondary market allows easy exit strategies, offering liquidity rarely found in real estate.

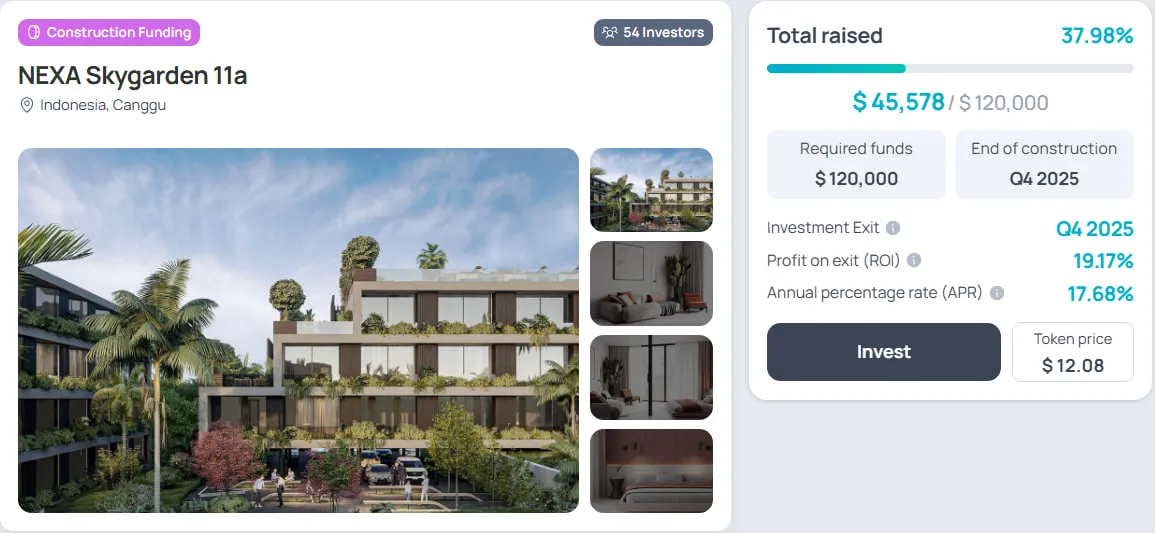

Nexa Sky Garden in Bali showcases how Binaryx provides unique opportunities. This property in Pererenan offers spacious, light-filled apartments designed for modern living. Nexa Sky Garden features amenities like an ocean-view pool, co-working spaces, and eco-friendly installations. With an entry point as low as $500, an expected construction ROI of around 19%, and a projected 15% rental APR, this investment blends high returns with a premium, exclusive location—making it an attractive inflation hedge.

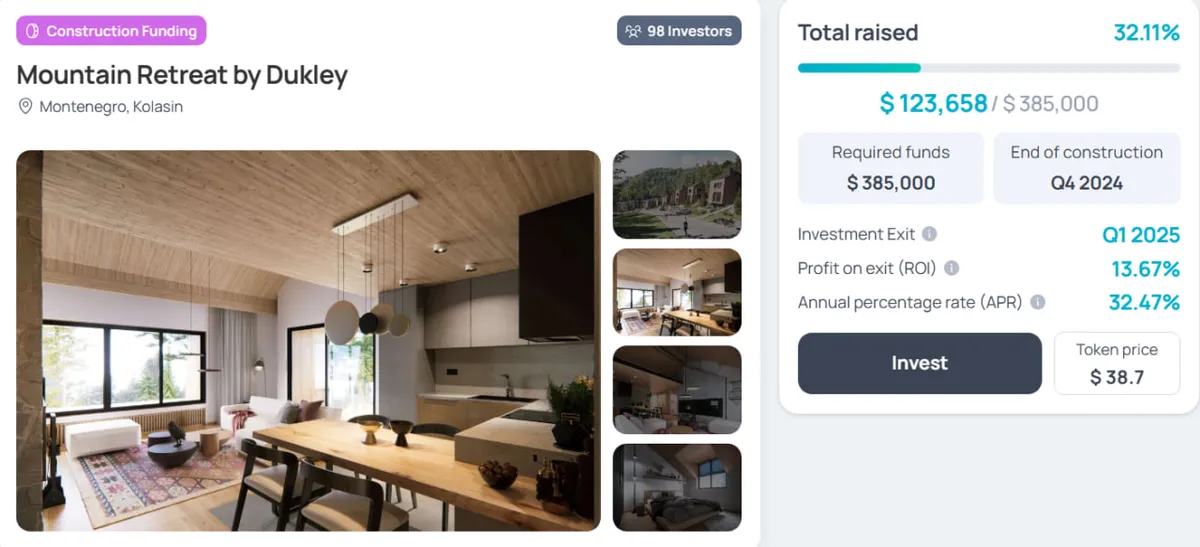

Mountain Retreat by Dukley in Montenegro adds another compelling option. Nestled between Kolasin and the Kolasin 1450 ski resort, this alpine-style complex offers chalets with modern amenities, including smart home systems and underground parking. The location is a year-round destination for winter sports and summer activities. With an investment horizon ending in Q1 2025 and an ROI exceeding 13%—translating to a 40%+ annualized return—Mountain Retreat combines exclusivity, strong yields, and a short-term investment period, showcasing how Binaryx can deliver on income and growth.

Final Thoughts

Inflation is a persistent, silent force that chips away at the value of your money, year after year. Protecting yourself against this financial erosion means looking at options that don’t just keep pace with inflation but outgrow it. While gold glimmers as a centuries-old safeguard and stocks offer steady long-term gains, real estate stands apart. It’s a tangible, income-generating asset and, with the right approach, a wealth amplifier.

Modern real estate investing has evolved, making it accessible even to those without massive upfront capital. Platforms like Binaryx open doors, blending the power of traditional property ownership with the ease of digital investments. Here, tokenization doesn’t just democratize access; it streamlines income distribution and liquidity, putting global real estate opportunities at your fingertips. Try it.