BlackRock's 4-Stage Tokenization Plan Explained

BlackRock's Vision of Tokenized Future

Quick Summary

BlackRock — the $10 trillion asset manager — projects every stock, bond, and real estate asset eventually moving onto blockchain through a four-stage progression: stablecoins, government bonds, expanding asset universe, then mass adoption. Tokenized real estate (Stage 4) is already deployable: the market is projected to grow from $3.5B in 2024 to $19.4B by 2033 (21% CAGR per Custom Market Insights), and retail investors can buy fractional shares of producing rental properties from $50 via platforms like Binaryx.

Larry Fink projected the future of the financial markets over the next several decades in January 2024. Following the approval of the Bitcoin ETF, the CEO of BlackRock made it clear: "every stock and bond would eventually live on a shared digital ledger." Coming from the head of a $10 trillion asset manager, these words are noteworthy; even more, they are a blueprint for finance's evolution.

The Numbers Behind the Vision

The figures illustrate the magnitude of the stakes. Global real estate tops $630 trillion. The bond market is approaching $150 trillion and growing, with government bonds making up 68% of that pie. Stock markets add $111 trillion. BlackRock sees these assets moving onto blockchain networks in the years ahead. Even if just 10% of real estate gets tokenized, that's $63 trillion in digital assets—three times bigger than today's entire crypto market. Add in a slice of stocks and bonds, and we're looking at a transformation worth hundreds of trillions.

Beyond Traditional Asset Classes

Beyond traditional markets, new asset classes keep emerging. Startups now tokenize everything from carbon credits and future athlete earnings to rare wines and intellectual property rights. Some platforms even let artists tokenize their creative works, while others focus on fractional ownership of luxury items like classic cars and fine art. These aren't just pilot projects—they're early examples of how blockchain could reshape what we consider investable assets.

The RWA 2025 Tokenization Report goes into great detail on these tendencies and possibilities. For a complementary view of how blockchain is reshaping property ownership specifically, see our explainer on how real estate meets blockchain. Now, let's explore how BlackRock plans to lead this financial transformation.

Current Leaders of Tokenization

The Institutional Shift

There has been a dramatic shift in the tokenization industry during the past 12 months. Conventional banking behemoths are now at the forefront, after having been long overshadowed by crypto natives. Launched in March 2024, BlackRock's BUIDL fund reached $520 million in 40 days—and that's not even scratching the surface. Franklin Templeton jumped in with their Benji fund, while Janus Henderson and Fidelity are busy doing their tokenized things.

Asset Class Breakdown Today

And what about the most heavily tokenized asset classes? Stablecoins, commonly referred to as tokenized fiat money, constitute 97% of all tokenized assets and have a market cap of $203 billion. U.S. Treasury bonds come second at $4 billion, followed by tokenized commodities at $1 billion—mostly in gold-backed tokens. Private credit sits at $575 million in active loans, while real estate and stocks are just getting started with $250 million and up to $70 million, respectively. Remember that these numbers might change quickly because the industry is always improving and measurement methods are always being tweaked. We obtained these data from our RWA 2025 Report, which explains how to calculate these estimations appropriately.

The Emerging Infrastructure Layer

For years, stablecoin titans such as Tether dominated tokenization; however, the landscape is changing. The market requires more diversified tokenized assets, which is where companies such as Securitize come in. Recently, BlackRock funded them $47 million to create infrastructure for institutional-grade tokenization. In stablecoins, government debt, and private credit markets, crypto pioneers such as MakerDAO and Ondo Finance—also supported by BlackRock—keep stretching limits. These players taken together are laying the groundwork for what Larry Fink called the "one general ledger" future.

Stages of World Tokenization (orchestrated by BlackRock)

The path to tokenizing the world's assets isn't random—it follows a logical progression that we can observe and map out. Let's break down these stages and see where we stand.

Stage 1: Digital Dollar Foundation (2014-2023)

Stablecoins solved a basic need—reliable digital money—which set the stage. Starting with Tether (USDT) and later joined by Circle (USDC), these tokens bridged the gap between traditional finance and blockchain. Some saw the early possibilities and started experimenting, while most big institutional actors observed from the sidelines. Two fundamental components were lacking during this time: unambiguous regulation and technology maturity (DeFi initially surfaced in 2020 and didn't fully hit its stride until late 2022).

Stage 2: Government Bond Revolution (2023-Present)

Here we are now, with BlackRock driving the change and crypto space fast institutionalizing under control. Launched in March 2024, their BUIDL fund broke ground as the first institutional-grade tokenized investment fund concentrating on US Treasury bonds. Franklin Templeton, Fidelity, and others quickly followed, driving tokenized Treasury bonds to $4 billion. The logic makes perfect sense: once you have stable digital money, you need safe places to park it. With the new US administration, regulatory barriers are starting to fall.

Stage 3: Expanding the Asset Universe

Here, we are witnessing the initial exploratory stages. Some platforms are now tokenizing private credit ($575 million), commodities ($1 billion), and even real estate ($250 million). Still, the sector struggles with basic issues like how best to handle money flows, tokenize various asset types, and control ownership rights. New structures are emerging through DAOs and specialized platforms like Securitize and Ondo Finance—both backed by BlackRock—but they're still mostly focused on stablecoins and bonds. Big players are laying groundwork for this stage while letting the market experiment, largely because demand and awareness haven't fully caught up yet.

Stage 4: Mass Adoption and Innovation

This is the endgame Larry Fink envisions—when tokenization becomes the default rather than the exception. Traditional assets will rapidly migrate to blockchain, while entirely new asset classes emerge. Yes, you'll find pioneers already tokenizing everything from wine collections to future athlete earnings, but don't let these early movers fool you—the institutional world still focuses on mastering government bonds. These innovators matter, but big money follows its own timeline. For a closer look at how the fractional ownership model that anchors Stage 4 actually works, see our complete guide to fractional real estate investing.

Are We Waiting for Regulations?

The Regulation Myth

The conventional wisdom suggests regulation is holding tokenization back. Yet reality paints a different picture. Take stablecoins—where market demand runs strong—regulatory frameworks barely matter. A full decade after Tether (USDT) hit the scene, the US is only now pushing its bipartisan Stablecoin Bill. For government bonds, current regulations aren't perfect, but they work well enough for giants like BlackRock to roll out products like BUIDL.

Real Estate: The Harder Problem

When we dive into more complex assets, things get interesting. Consider real estate tokenization: the real challenge isn't just regulation—it's cracking the code on fractional ownership, cross-border deals, and digital custody rights, then convincing people it's both safe and worthwhile. We already have promising local initiatives, like Wyoming's 2021 DAO LLC SF0038 act, which created structures perfect for real estate tokenization.

Demand Leads, Rules Follow

Sometimes market demand and maturation are all we need. Stablecoins prove this point—they exploded to $203 billion because the market wanted them, and regulators simply adapted. Other asset classes might follow the same path. BlackRock isn't sitting around waiting for perfect regulations; they're actively building infrastructure through investments in companies like Securitize while the regulatory landscape catches up.

So what's really holding us back? Not just regulations, but market maturity. We need better digital identity solutions, streamlined KYC/AML processes, and most crucially, genuine demand from users who get these products. The regulatory framework will naturally evolve as the market proves what works. Meanwhile, smart players are laying the groundwork, knowing that rules follow innovation, not the other way around.

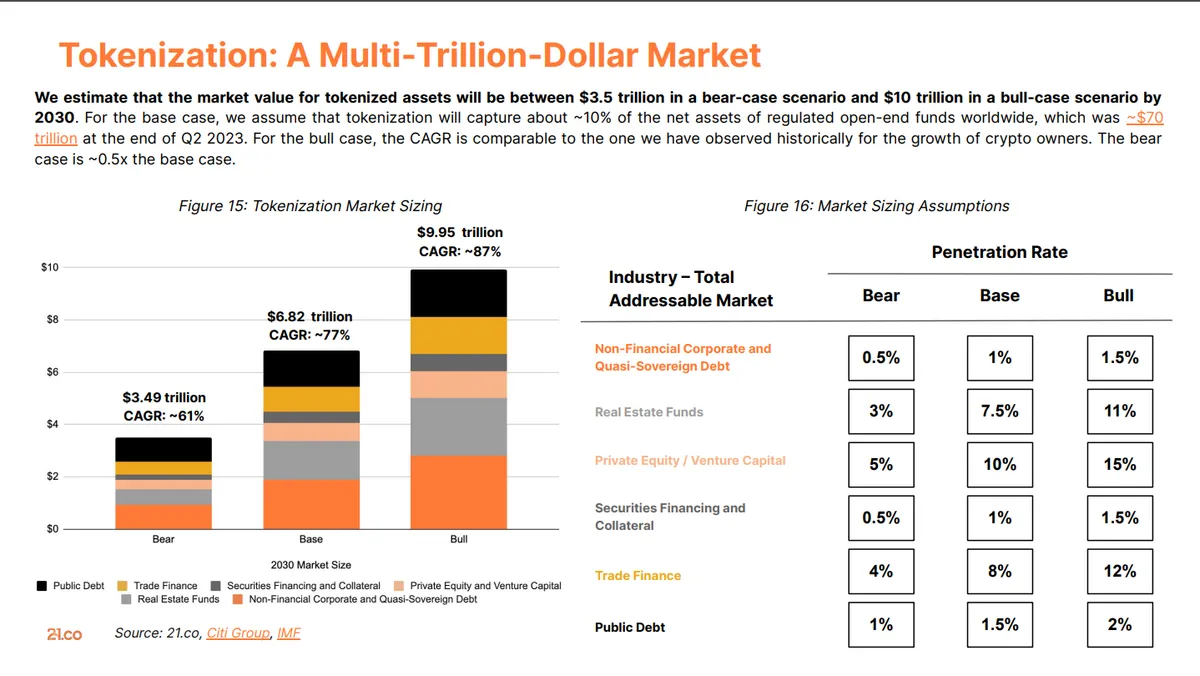

Quantitative Projections of Tokenization by 2030

The Untokenized Pool

Let's look at hard numbers. Today's tokenized assets total around $209 billion, with stablecoins making up $203 billion of that pie. But to understand where we're heading, we need to look at the massive markets waiting to be tokenized: $630 trillion in real estate, $150 trillion in bonds, and $111 trillion in global equities.

Base Case vs. Bull Case Through 2030

Conservative estimates put tokenized assets at $3.5 trillion by 2030, while optimistic projections reach $10 trillion. This wide range makes sense when you break down different adoption scenarios:

Base Case ($3.5 trillion):

- Roughly 10% of regulated fund assets move to blockchain

- Institutional investors adopt at a steady, measured pace

- Focus stays on familiar territory: bonds, commodities, and other traditional assets

Bull Case ($10 trillion):

- Banks and funds move faster, driven by significant cost savings

- Real estate tokenization catches fire—even a modest 1% would add $6.3 trillion

- New asset classes emerge and quickly gain market acceptance

These aren't just numbers pulled from thin air. We base them on current growth rates, institutional moves like BlackRock's BUIDL fund, and real market demand. The real question isn't if we'll hit these numbers, but when. For deeper geographic context on which countries are absorbing this growth fastest, see our analysis of the best countries to invest in real estate in 2026.

How to Participate in Tokenization?

Stablecoins as Your Entry Point

Your starting point into tokenization is mostly determined by the assets that interest you. Congratulations, if you already utilize stablecoins for payments or trading—you are now a member of the tokenization revolution. If you're seeking something more intriguing, though, there are various possibilities. Our guide to investing in tokenized real-world assets maps that exact route, from stablecoins all the way to real estate.

Government Bond Funds

For those who are interested in government bonds, institutional-grade funds such as Franklin Templeton's Benji or BlackRock's BUIDL provide exposure to tokenized U.S. Treasuries.

Tokenized Equities and Other Instruments

For those drawn to other asset classes, choices are growing. Companies like Hashnote concentrate on tokenized financial instruments; platforms like Backed Finance provide tokenized stocks. The secret is performing extensive study and knowing exactly what rights and protections your tokens grant.

Tokenized Real Estate via Binaryx

Real estate tokenization gives another intriguing option. Operating under Wyoming's 2021 legislation (W.S. SF0038), Binaryx is one platform making this easily available. We create a dedicated Wyoming LLC for each property, which then issues blockchain tokens. When you buy these tokens, you become a co-owner of the LLC that owns the property, with your ownership rights protected by state law. To compare the on-chain model side by side with the conventional one, read our tokenized vs. traditional real estate breakdown, or see how this fits into a wider hands-off allocation in our passive income real estate guide. And when you are ready to act, our walkthrough of buying tokenized real estate covers every step from account setup to your first rent payout.

Deep Dives and References

Want to dive deeper? Check out these resources:

- Binaryx Legal Guide: How the Platform Ensures Investor Protection

- What to Do if Binaryx Disappears: The Fate of Your Tokens and Action Plan

- Our comprehensive RWA 2025 Report for detailed market analysis

Frequently Asked Questions

What is BlackRock's tokenization vision?

BlackRock CEO Larry Fink projects that "every stock and bond would eventually live on a shared digital ledger." The vision unfolds across four stages: Stage 1 stablecoins (2014-2023), Stage 2 government bonds (2023 onward, led by the BUIDL fund), Stage 3 expanding into real estate, private credit, and commodities, then Stage 4 mass adoption across all asset classes. BlackRock isn't waiting for perfect regulation — it is actively building infrastructure through investments in Securitize, Ondo Finance, and similar platforms.

Is real estate already being tokenized?

Yes. The tokenized real estate market is projected to grow from $3.5 billion in 2024 to $19.4 billion by 2033, a 21% compound annual growth rate per Custom Market Insights. Platforms like Binaryx tokenize physical rental villas in Bali, Montenegro, and Turkey under a Wyoming DAO LLC structure. Investors buy fractional shares from $50 and receive proportional rental income on-chain.

How is tokenized real estate different from REITs?

A REIT is a publicly listed company holding a portfolio of properties — you buy shares of the trust, not the buildings. With tokenized real estate, each token represents fractional ownership in a specific identifiable property held by a dedicated LLC. You know exactly which villa or building your money supports, you receive rent directly proportional to your stake, and on-chain settlement removes most intermediaries from the income flow.

Can retail investors participate in tokenized real estate?

Yes. Unlike BlackRock's BUIDL fund (institutional only) or many tokenized Treasury products (accreditation gates), tokenized real estate platforms like Binaryx accept retail investors with no accreditation requirement. Entry starts at $50 per token, and rental yield is paid out monthly on-chain. This makes Stage 4 retail-accessible today, ahead of the broader institutional rollout for stocks and bonds.

What is the timeline for full real estate tokenization?

Realistically, mid-decade for institutional scale (2027-2030) and the full BlackRock 4-stage vision likely runs through 2035. The bottleneck is not regulation alone but also digital identity infrastructure, KYC/AML standardization, and demand maturity. That said, retail-grade real estate tokenization is already operational — investors don't need to wait for the institutional curve to catch up before participating.

Which blockchains are leading real estate tokenization?

Ethereum dominates institutional tokenization (BlackRock's BUIDL fund launched on Ethereum) thanks to its mature smart contract ecosystem and largest validator set. Polygon is widely used for retail-facing real estate platforms because of low transaction fees. Other chains making inroads include Avalanche, Stellar, and Solana for specific use cases. Most platforms abstract the underlying chain so investors interact with a familiar dashboard rather than directly with the blockchain.

Invest in Tokenized Real Estate Today

BlackRock's 4-stage vision will take years to play out for stocks and bonds. But Stage 4 — real estate tokenization — is already deployable. Binaryx tokenizes high-yield international rental properties under a Wyoming DAO LLC framework, settling rent on-chain in stablecoins. Investors already collecting that rent share their numbers in our customer testimonials and success stories.

Want to participate in Stage 4 today? Browse Binaryx tokenized rental properties across Bali, Montenegro, and Turkey. Or open a Binaryx account and start with $50.

Read more:

- Fractional Real Estate Investing: 2026 Complete Guide — companion deep-dive on the legal structure

- Passive Income Real Estate: 6 Proven Ways to Start in 2026 — broader survey of RE income strategies

- 8 Best Countries to Invest in Real Estate in 2026 — international markets ranked

- RWA Market 2026: Tokenization on Track for $10T — broader RWA tokenization outlook

This article is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. All investments carry risk, including potential loss of principal.